Navigating Rising Rates in Corporate Credit

Monetary policy is changing as central banks navigate the new era of quantitative tightening amid geopolitical tensions, rising inflation, and elevated recession concerns. In this Q&A, portfolio manager Lillian Lin and product strategist Philipp Nowak discuss why a low-duration approach may be an attractive solution for investors seeking credit exposure in today’s markets.

Q: What are the implications for credit investors of a rising rate environment?

Lin: While the rates market is pricing in several hikes, yields have already increased materially and bonds are looking more attractive overall. We believe this is particularly relevant today, as investors’ focus is progressively shifting from inflation to growth and recession risk. Although PIMCO is constructive on the outlook for investment grade (IG) credit (we expect investment grade credit fundamentals to remain resilient in 2022), we cannot rule out a period of protracted volatility ahead in rates and spreads. In this context, we believe low-duration IG corporate bonds may represent an interesting value proposition for investors who are concerned about protracted rate and spread volatility, as these provide attractive carry with generally more limited downside risk compared to longer-dated bonds.

Q: What are the key potential benefits of short-dated corporate bonds?

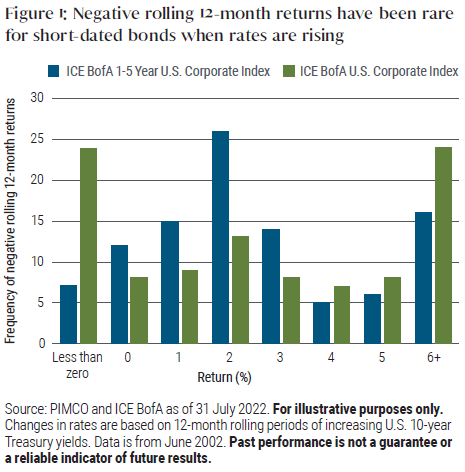

Lin: Short-dated corporate bonds may reduce interest rate sensitivity and have the potential to outperform long-dated Treasuries and the broad corporate market when rising interest rates spur market volatility. Short-dated corporate bonds have historically posted higher Sharpe ratios than intermediate or long-dated corporate bonds, indicating a generally more favorable risk-adjusted return profile. These bonds occupy a unique part of the credit curve where the duration is close to the yield. With a duration typically between two to three years, the ICE BofA Merrill Lynch 1-5 Year US Corporate Index has less than half the interest rate sensitivity of the full corporate bond universe and therefore will likely be less affected when rates rise. Moreover, given the higher yield per unit of duration for this index, it tends to more quickly reverse losses prompted by rising rates. This leads to fewer negative rolling 12-month returns during periods of rising rates (see Figure 1).

Short-dated corporate bonds also offer higher income than government bonds of similar maturity and can be a more defensive way to take credit exposure. As an example, looking at the past 20 years, the maximum drawdown of the ICE BofA 1-5 Year US Corporate Index was approximately 60% of the full- maturity credit index, represented by the ICE BofA US Corporate Index. The most recently experienced sell-offs caused by COVID-19 and the Russian invasion of Ukraine – which ranked the second and third biggest, respectively, of the past two decades – reaffirmed the more defensive nature of the lower-duration index. Its drawdown has been about half of the drawdown of the full-maturity index on both occasions. In this context, short-duration corporate bonds can offer a number of potential advantages including income, liquidity, and reduced volatility compared to longer-dated bonds.

Q: What are some of the potential risks?

Nowak: Investors should remember that short-duration corporate bonds are not risk free. As with other corporate bonds, they have credit or default risk – the risk that the borrower fails to repay and defaults on its obligation. However, although not immune to default risk, the default rate of IG companies has historically been close to 0%, according to data from Moody’s.

In addition to the lower default risk of an IG strategy, PIMCO’s independent credit research seeks to invest in resilient companies with strong fundamentals, further reducing the risk of permanent capital losses. Investors in short-duration corporate bonds are also subject to spread risk, which is the risk that credit spreads (the difference between U.S. Treasury and corporate bond yields) widen, and although short dated, they may still be exposed to potential losses if interest rates continue to rise. PIMCO seeks to mitigate these risks via robust credit research and an active investment approach.

Q: What is PIMCO’s process for selecting short-dated corporate bonds?

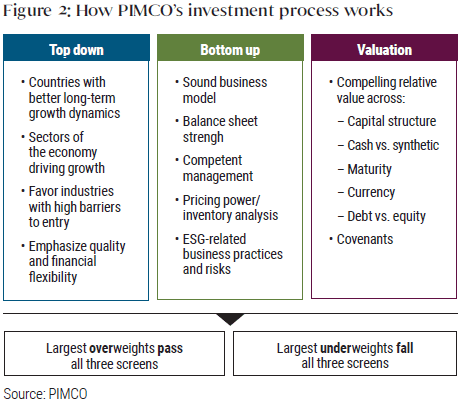

Nowak: PIMCO’s approach to investing in short-dated corporate bonds involves a three-step process in which we evaluate top-down considerations, bottom-up fundamentals, and valuations (see Figure 2). Through this process, we aim to identify sectors and companies with high barriers to entry, superior growth potential, strong pricing power, favorable asset quality, and management teams that support bondholders. The process is anchored by PIMCO’s Secular and Cyclical Forum process, which provides the framework for overall industry allocations, the level of credit risk, as well as duration positioning.

In addition, our global investment team – supported by more than 80 credit analysts located across North and South America, Europe, and Asia – enables us to perform in-depth bottom-up credit research, thereby seeking to reduce default risk and avoid overvalued credits. Moreover, as a large lender, PIMCO offers the distinct advantage of being able to engage in reverse inquiries, where a company approaches us directly with a proposal for a potential investment or we approach the company and act as an anchor investor in a bond issuance. Conducting reverse inquiries helps PIMCO to provide financing at spread levels we deem attractive given our view on company fundamentals. Directly negotiating also means PIMCO could potentially impact the structure of new issues, such as covenants or level of debt seniority.

Q: How can an active approach potentially enhance yields?

Lin: Shifting to a low-duration strategy typically involves a compromise: Yields may be attractive on a risk-adjusted basis, but they tend to be lower than the broader market. An active strategy can help to narrow this gap and provide a yield closer to that of full-maturity credit, with much lower duration. For example, PIMCO US Low Duration Corporate Bond UCITS ETF currently has a yield of 4.3%, which is similar to that of the full-maturity ICE BofA US Corporate index of 4.4% while having less than half the duration (as of 31 July 2022). We attribute this to our focus on identifying particular sectors and specific issuers that offer opportunities for enhancing yield while avoiding segments of the market that we view as unattractive on a risk-adjusted basis.

From a positioning standpoint, we remain selective on generic credit and look to apply bottom-up ideas to emphasize “bend but don’t break” positions. The widening in spreads since the beginning of the year has led to an improvement in valuations, while dispersion across sectors and issuers continues to offer active management opportunities. COVID-impacted sectors, select BBBs, new issues, sectors that benefit from rising rates, issuers with strong pricing power, and rising stars potentially offer upside and are therefore an area of focus for PIMCO US Low Duration Corporate Bond UCITS ETF. We are underweight non-cyclical issuers with tight spreads and limited upside; we’re also seeking to avoid re-leveraging risk in sectors such as pharmaceuticals and food and beverage. Similarly, we also maintain a cautious approach in secularly challenged sectors such as retail.

Q: How can short-dated corporates help navigate a rising rate environment?

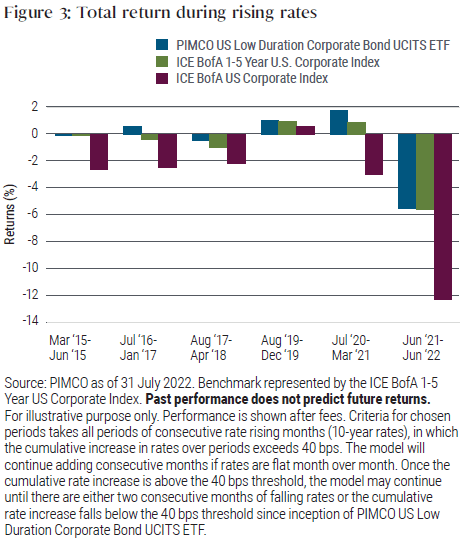

Nowak: Short-dated corporates have a structurally lower duration, which helps to naturally defend against rising rates, as we highlighted in Figure 1. In addition, those investors looking to embrace an active management approach can benefit further by investing in PIMCO US Low Duration Corporate Bond UCITS ETF, which has the ability to adjust duration between zero and four years depending on our forecast for interest rates. This allows PIMCO to potentially limit the downside impact of interest rate changes even further when we anticipate higher rates. The low-duration tilt of the strategy – together with an active management approach – has allowed the ETF to successfully navigate rising rate environments, outperforming its benchmark over different periods of rising rates (Figure 3).

Moreover, the strategy’s focus on credit instruments means that it will empirically behave as if it has less interest rate risk than might be initially estimated. This is because factors other than interest rate movements, such as credit spreads, will drive price fluctuations. Given our focus on companies and industries that are experiencing above-average growth, improving fundamentals and have potential for tightening spreads, investors may still be rewarded with bond price appreciation even if interest rates were to rise.

Q: Where could the fund fit in an investors’ portfolio?

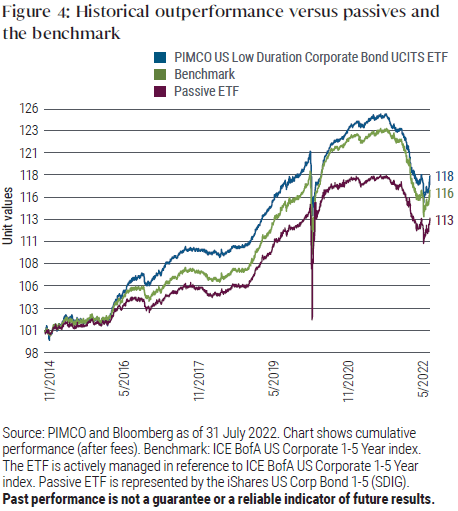

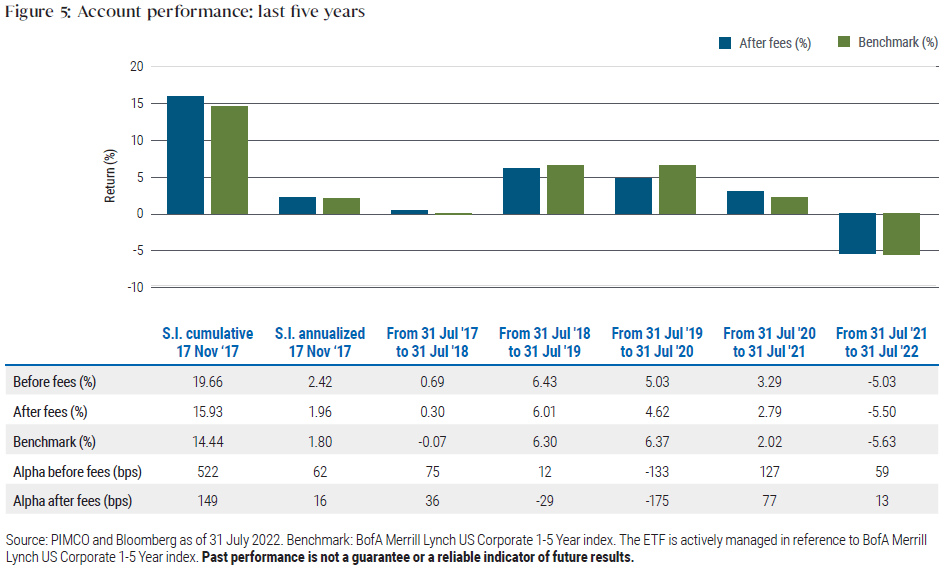

Nowak: PIMCO US Low Duration Corporate Bond UCITS ETF offers a potential solution for actively managing the impact of higher U.S. interest rates. Specifically, it may fit within an investor’s low-duration fixed income allocation. The strategy will typically have more risk and volatility than a traditional low-duration government portfolio; however, investors with exposure to short-term government bonds may consider moving part of this allocation into credit to diversify their exposure while seeking to maintain elevated yields. Alternatively, the strategy might be used by investors who are looking to allocate to high quality credit given the more attractive valuations compared to the start of the year, while limiting their duration exposure and the price volatility of their investment. Due to its actively managed investment approach, the PIMCO US Low Duration Corporate Bond UCITS ETF has meaningfully outperformed its benchmark as well as passively managed products since inception of the strategy in 2014 (see Figure 4).

Important information

Featured Participants

Disclosures

Marketing Communication

This is a marketing communication. This is not a contractually binding document and its issuance is not mandated under any law or regulation of the European Union or the United Kingdom. This marketing communication does not include sufficient detail to enable the recipient to make an informed investment decision. Please refer to the Prospectus of the UCITS and to the KIID before making any final investment decisions.

For professional use only

The services and products described in this communication are only available to professional clients as defined in the MiFiD II Directive 2014/65/EU Annex II Handbook and its implementation of local rules. This communication is not a public offer and individual investors should not rely on this document. Opinion and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness.

PIMCO Europe Ltd (Company No. 2604517) is authorised and regulated by the Financial Conduct Authority (12 Endeavour Square, London E20 1JN) in the UK. The services provided by PIMCO Europe Ltd are not available to retail investors, who should not rely on this communication but contact their financial adviser. PIMCO Europe GmbH (Company No. 192083, Seidlstr. 24-24a, 80335 Munich, Germany), PIMCO Europe GmbH Italian Branch (Company No. 10005170963), PIMCO Europe GmbH Irish Branch (Company No. 909462), PIMCO Europe GmbH UK Branch (Company No. 2604517) and PIMCO Europe GmbH Spanish Branch (N.I.F. W2765338E) are authorised and regulated by the German Federal Financial Supervisory Authority (BaFin) (Marie- Curie-Str. 24-28, 60439 Frankfurt am Main) in Germany in accordance with Section 15 of the German Securities Institutions Act (WpIG). The Italian Branch, Irish Branch, UK Branch and Spanish Branch are additionally supervised by: (1) Italian Branch: the Commissione Nazionale per le Società e la Borsa (CONSOB) in accordance with Article 27 of the Italian Consolidated Financial Act; (2) Irish Branch: the Central Bank of Ireland in accordance with Regulation 43 of the European Union (Markets in Financial Instruments) Regulations 2017, as amended; (3) UK Branch: the Financial Conduct Authority; and (4) Spanish Branch: the Comisión Nacional del Mercado de Valores (CNMV) in accordance with obligations stipulated in articles 168 and 203 to 224, as well as obligations contained in Tile V, Section I of the Law on the Securities Market (LSM) and in articles 111, 114 and 117 of Royal Decree 217/2008, respectively. The services provided by PIMCO Europe GmbH are available only to professional clients as defined in Section 67 para. 2 German Securities Trading Act (WpHG). They are not available to individual investors, who should not rely on this communication.| PIMCO (Schweiz) GmbH (registered in Switzerland, Company No. CH-020.4.038.582-2). The services provided by PIMCO (Schweiz) GmbH are not available to retail investors, who should not rely on this communication but contact their financial adviser.

Additional Information/Documentation

A Prospectus is available for PIMCO Funds and Key Investor Information Documents (KIIDs) are available for each share class of each the sub-funds of the Company.

The Company’s Prospectus can be obtained from www.fundinfo.com and is available in English, French, German, Italian, Portuguese and Spanish.

The KIIDs can be obtained from www.fundinfo.com and are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive).

In addition, a summary of investor rights is available from www.pimco.com.The summary is available in English.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. PIMCO Global Advisors (Ireland) Limited can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.”

This presentation contains the current opinions of the manager and such opinions are subject to change without notice. This presentation has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this presentation may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2022, PIMCO.